Swati Balani is a purpose-driven leader, certified Independent Director (IICA), and passionate advocate for sustainability, social equity, zero hunger and holistic well-being. A certified professional from Harvard Business School Online’s Leadership and Sustainability programs, she blends global insights with grassroots action to advance the United Nations Sustainable Development Goals (SDGs).

With nearly two decades of corporate experience, Swati is dedicated to creating meaningful impact across key areas—gender equality, environmental consciousness, and inclusive growth. Through her wellness initiative, SoulSyncWellness.HowWhatWhy.com, she actively promotes SDG 3: Good Health & Well-being, offering resources, guidance, and community support for physical, emotional, and spiritual health. Similarly she actively works on spreading awareness to reduce hunger, poverty, gender inequality, CO2 emissions to save the planet.

Having witnessed the challenges of inequality and wellness neglect, Swati believes that even small, mindful actions can spark powerful, collective change. Her mission is clear: to help build a more conscious, compassionate, and sustainable world—one step, one voice, one life at a time.

At 4:30 pm on a Friday, the office conference room slowly fills up.

Pink balloons hang from the ceiling. A cake sits in the center of the table.

Someone announces, “Happy Women’s Day everyone!”

The team claps. Photos are taken. The cake is cut. The HR manager gives a short speech about “empowering women in the workplace.”

Everyone smiles.

But on Monday morning, the same office quietly returns to normal.

The same women who cut the cake:

• are passed over for promotions and kept in lower roles than men • are often paid less for the same work, due to pay gap bias and belief men are primary earners • see their ideas ignored in meetings, until repeated by a man • are called “too emotional” or “difficult” when they question decisions • are denied leadership roles due to assumptions about marriage, motherhood, childcare • face bias around late-night work, travel, relocation expectations

Many struggle to grow due to: • male-dominated leadership networks where promotions circulate among men • encounter conscious and unconscious gender bias in hiring and evaluations • face male ego barriers when women challenge or lead men • are judged by traditional norms expecting men to lead • double burden of career and family responsibilities while proving commitment

Many quickly learn the unspoken rule of survival:

The safest way to succeed is to say “yes” to male bosses.

Independent thinking is often seen as difficult. Disagreement is seen as disrespect. Leadership is seen as aggression.

And yet, every year we celebrate International Women’s Day.

But this day was never meant to be about cakes, flowers, or corporate photo sessions.

It was born from struggle, courage, and a demand for equality and women are still struggling for equality.

How Women’s Day Began: A Movement, Not a Celebration

International Women’s Day traces its origins to the early 1900s, when women workers across Europe and the United States began protesting against poor working conditions, low wages, and lack of political rights.

In 1917, women in Russia went on strike demanding “Bread and Peace.” Their protest became a powerful turning point in history and March 8 later became associated with women’s struggles for justice.

Decades later, the United Nations officially recognized International Women’s Day in 1977, giving global legitimacy to the movement.

Since then, March 8 has become a day to recognize women’s achievements while reminding the world that equality is still unfinished business.

Milestones That Changed Women’s Rights

Progress for women has come step by step through decades of activism.

Global milestones

1893 – New Zealand becomes the first country to grant women voting rights

1945 – The UN Charter recognizes equality between men and women

1975 – UN declares International Women’s Year

1977 – UN formally recognizes International Women’s Day

1993 – UN Declaration on Elimination of Violence Against Women

Milestones in India

India too has seen powerful progress:

1917 – Indian women demand voting rights during British rule

1950 – The Indian Constitution guarantees equal voting rights

1966 – India elects its first woman Prime Minister

2005 – Domestic Violence Act strengthens legal protection for women

Growing participation of women in entrepreneurship, science, governance, and sports

But progress has been uneven.

And many challenges remain.

The Silent Crisis: Domestic Violence

While corporate discussions focus on leadership and diversity, millions of women are still fighting for something far more basic — safety in their own homes.

Globally, 1 in 3 women experience physical or sexual violence during their lifetime, most often from an intimate partner.

Many cases go unreported due to:

fear

financial dependence

social stigma

pressure to “protect family honour”

Domestic violence is not limited to physical abuse.

It also includes:

emotional control

financial restriction

intimidation and psychological manipulation

For many women, the most dangerous place is not the street — but their own home.

The Gender Gap: Where the World Stands

Despite decades of progress, gender equality remains far from reality.

According to the Global Gender Gap Report, the world has closed only about 68% of the gender gap.

Countries leading in gender equality include:

Iceland

Finland

Norway

New Zealand

United Kingdom

These countries perform well because of:

equal pay policies

parental leave for both parents

higher representation of women in leadership

strong laws against discrimination

Where India Stands

India ranked 131 out of 148 countries in the Global Gender Gap Report 2025.

The biggest challenges remain in:

economic participation

wage equality

leadership representation

Even today, many workplaces still struggle with:

fewer women in senior roles

gender bias in promotions

unequal pay for similar work

This shows that economic growth alone does not guarantee gender equality.

Social attitudes must change too.

From Pain to Power: Indian Women Who Broke Barriers

Despite challenges, countless women have risen above adversity and rewritten the rules.

Their stories show what is possible when courage meets opportunity.

Kalpana Chawla – From a Small Town to Space

Born in Karnal, Haryana, Kalpana Chawla grew up in a time when aerospace engineering was considered a male domain.

Yet she pursued her dream relentlessly, eventually becoming an astronaut at NASA.

In 1997 she became the first woman of Indian origin to travel to space.

Her life showed millions of girls that dreams are not limited by geography or gender.

Kiran Mazumdar-Shaw – Building a Global Biotech Company

When Kiran Mazumdar-Shaw started her career, banks refused to lend to her because she was a young woman entrepreneur.

Undeterred, she started a small biotechnology company in a garage.

That company later became Biocon, one of India’s leading biotech firms.

Her journey transformed her from a struggling entrepreneur to one of the most influential business leaders in India.

Mary Kom – Fighting Inside and Outside the Ring

Growing up in rural Manipur, Mary Kom faced poverty, social barriers, and skepticism about women in boxing.

Yet she persevered.

She went on to become a six-time world boxing champion and Olympic medalist.

Her story is proof that strength has nothing to do with gender.

An Often Ignored Truth: Women Must Support Women

While many barriers come from society, another challenge sometimes comes from within our own circles.

Too often, women are pushed into competing for limited opportunities.

This can create:

jealousy

unhealthy competition

lack of mentorship

But real progress happens when women move from competition to collaboration.

When women support each other:

workplaces become more inclusive

leadership pipelines become stronger

younger women gain confidence to rise

The success of one woman should not be seen as a threat.

It should be seen as a door opening for many others.

The Real Call to Action

International Women’s Day should not end with a cake or a social media post.

It should inspire real change.

Governments must

strengthen laws against domestic violence

ensure equal pay and workplace protections

increase women’s political representation

Organizations must

promote women based on merit

create inclusive leadership cultures

eliminate bias in hiring and promotions

Men must

become allies in equality

challenge discrimination

support women’s leadership

And women must

support other women instead of competing destructively

mentor younger women

celebrate each other’s achievements

speak up against injustice

The Question Every Workplace Must Ask

When the cake is cut and the photos are posted, every organization should pause and ask:

Are we celebrating women — or truly empowering them?

Because the true spirit of International Women’s Day lies not in celebration.

It lies in creating a world where:

a woman’s voice is heard

her ideas are respected

her safety is protected

her leadership is welcomed

And where women stand not against each other — but together.

ESG India 2025 — A Year That Began With Confidence

At the beginning of 2025, ESG in India felt quietly optimistic.

There was a growing belief that the foundations were finally in place. Sustainability had moved beyond slogans and speeches. Board agendas carried ESG as a standing item. BRSR disclosures brought structure and comparability. Climate targets, social commitments, and governance frameworks appeared more disciplined than ever before.

In newspapers and business forums, ESG was largely reported as a success story. Indian corporates were portrayed as maturing — learning from past missteps and aligning with global expectations. Water stewardship, renewable energy, electric mobility, diversity goals — these were no longer peripheral ideas. They had entered the mainstream.

The narrative was reassuring. ESG had arrived.

Yet, as the year unfolded, that confidence was quietly tested.

Not through one dramatic collapse — but through a series of small, human, and operational moments that rarely dominate headlines. A workforce reduction described as restructuring. A supplier incident framed as operational disruption. A community concern deferred. A climate ambition stated without a visible transition pathway.

Individually, these moments appeared manageable. Collectively, they told a different story.

By the end of 2025, ESG in India no longer felt like a destination reached. It felt like a system under strain.

What changed was not intent — but pressure. Pressure from regulators asking sharper questions. Pressure from investors connecting disclosures with decisions. Pressure from employees and communities expecting consistency between values and behaviour.

2025 did not end with the failure of ESG. It ended with a warning.

A warning that ESG cannot live only in reports. A warning that governance determines whether sustainability survives stress. A warning that trust, once tested, demands proof — not persuasion.

And yet, there is reason for hope.

Because 2025 clarified what truly matters. It revealed that ESG works when embedded in decisions, not narratives. It showed that accountability strengthens credibility. It reminded boards that sustainability is measured not by ambition — but by behaviour when choices are difficult.

As India steps into 2026, ESG stands at a crossroads. One path leads back to comfort and optics. The other leads forward — toward discipline, honesty, and resilience.

1. 2025: When ESG Moved From Narrative to Governance Reality

As 2025 progressed, ESG stopped behaving like a reporting exercise and began asserting itself as a governance issue.

With SEBI’s Business Responsibility and Sustainability Reporting (BRSR) framework firmly in force, ESG disclosures now required:

Formal board approval

Cross-functional data ownership

Explicit accountability for accuracy

From an Independent Director lens, the implication was unambiguous:

Once ESG disclosures are approved by the board, ESG risk becomes a fiduciary responsibility — not a sustainability team activity.

2025 did not simplify ESG. It removed plausible deniability.

2. Environmental ESG: Where India Demonstrated Real Progress

2.1 ITC: Water Stewardship as Risk Management

ITC continued to be cited in public disclosures for its long-term leadership in water stewardship.

Initiatives publicly reported included:

Large-scale watershed development

Rainwater harvesting across manufacturing sites

Integration of water security into agricultural supply chains

The governance lesson was clear: environmental leadership gains credibility when it protects business continuity, not just reputation.

2.2 Tata Group & Tata Motors: Climate Action Backed by Capital

Across Tata Group companies, climate ambition in 2025 was increasingly visible through investment decisions.

Tata Power expanded renewable capacity.

Tata Steel disclosed transition risks while piloting decarbonisation pathways.

Tata Motors strengthened its EV roadmap, directly linking sustainability with future mobility and competitiveness.

Capital followed intent — and markets noticed.

2.3 Mahindra & Mahindra: EV Innovation as Strategic ESG

Mahindra & Mahindra (M&M) emerged as a strong example of ESG aligned with innovation.

Public announcements highlighted:

Expansion of electric vehicle portfolios

Investments in dedicated EV platforms

Positioning sustainability as a growth opportunity rather than a compliance cost

This reinforced a central ESG truth: sustainability delivers value when embedded in core strategy.

2.4 Infosys: Carbon Neutrality With Disclosure Discipline

Infosys continued to receive attention for its progress toward carbon neutrality.

Public disclosures reflected:

High renewable energy adoption

Energy efficiency initiatives

Transparent acknowledgement of Scope 3 limitations

Credibility was built through honesty, not perfection.

3. Environmental ESG: Where Gaps Became Visible

3.1 Heavy Industry and the Scope 3 Constraint

Industrial groups such as JSW demonstrated progress on emissions efficiency and renewable sourcing.

Yet public disclosures and analyst commentary continued to highlight:

Supplier readiness gaps

Inconsistent Scope 3 data

Limited influence beyond direct operations

2025 reinforced a structural constraint:

Climate strategies limited to owned assets remain incomplete.

3.2 Net-Zero Without Transition Pathways

Across sectors, net-zero commitments often lacked:

Interim milestones

Clear capex linkage

Operational accountability

By year-end, public scrutiny increasingly questioned ambition without execution.

4. Social ESG: Layoffs, Labour, and Livelihoods

If environmental ESG was tested by capital allocation, Social ESG in 2025 was tested by people decisions.

4.1 Layoffs: The Defining Social ESG Moment of 2025

Across IT, startups, and new-age companies, layoffs emerged as the most visible ESG stress test of the year.

Public disclosures and media reports revealed:

Workforce reductions framed as efficiency or restructuring

Limited transparency on decision criteria

Inconsistent transition support for affected employees

From a governance lens, uncomfortable questions emerged:

Were social impacts debated at board level?

Were reskilling or redeployment meaningfully explored?

Did workforce decisions align with stated ESG values?

2025 showed that how layoffs are executed matters as much as why they occur.

4.2 Supply Chains and the Vedanta-Type Reality

In extractive and heavy industries — illustrated by Vedanta-type ecosystems — social risks continued to originate in contractor and supplier networks.

Public reporting highlighted:

Worker safety incidents

Contract labour vulnerabilities

Community trust deficits

A recurring lesson emerged:

Most social ESG failures occur where oversight is weakest — beyond direct payrolls.

4.3 Services Sector: Inclusion Beyond Numbers

In IT and services companies, gender diversity metrics improved.

However, public signals — attrition data, employee sentiment, and media reporting — pointed to unresolved challenges:

Burnout

Middle-management inclusion gaps

Psychological safety concerns

Representation improved. Inclusion maturity remained uneven.

5. Governance (G): Progress With Persistent Weaknesses

5.1 BRSR as a Structural Governance Win

BRSR fundamentally changed ESG oversight by enforcing:

Formal ownership

Board accountability

Disclosure discipline

ESG could no longer be treated as optional.

5.2 ESG Data Quality: The Silent Governance Risk

At the same time, 2025 exposed weaknesses:

Manual data collection

Weak internal controls

Inconsistent definitions

Boards increasingly faced discomfort signing off ESG disclosures without financial-grade assurance.

5.3 The Expanding Role of Independent Directors

Public scrutiny reshaped expectations from independent directors:

Passive endorsement is no longer acceptable

Inquiry and escalation are expected

Silence increasingly carries reputational risk

Independence without engagement proved insufficient.

6. How ESG Looked at the End of 2025

By December 2025, ESG no longer felt reassuring.

Headlines shifted from commitments to consequences.

ESG Performance Across Indian Sectors in 2025: What Held, What Cracked, What Must Change

By the end of 2025, it became evident that ESG performance in India did not move uniformly. Each sector revealed a different relationship with environmental limits, social responsibility, and governance discipline.

From an Independent Director lens, ESG in 2025 looked less like a single journey—and more like many parallel stress tests.

1. Energy & Power: Strong Momentum, Uneven Transition

What went well

Rapid expansion of renewable capacity (solar, wind, hybrid)

Greater disclosure on transition risks and stranded assets

Improved alignment between climate goals and capital allocation

Visible examples

Tata Power’s renewable expansion

Adani Green’s scale-driven clean energy push

NTPC’s gradual but visible transition narrative

What struggled

Coal dependence remained high

Just transition planning for workers and communities was weak

Grid stability and storage lagged ambition

ID lens takeaway

India’s energy transition progressed—but governance around social transition lagged behind environmental ambition.

2. Metals, Mining & Cement: Environmental Progress, Social Fragility

What went well

Energy efficiency improvements

Increased renewable sourcing

Better emissions monitoring and disclosure

Visible examples

JSW Steel’s efficiency measures

Tata Steel’s decarbonisation pilots

Cement majors investing in blended cement and waste heat recovery

What failed

Contractor safety incidents

Community trust deficits

Labour and rehabilitation challenges (Vedanta-type situations)

ID lens takeaway

In heavy industry, ESG failure in 2025 was rarely environmental—it was social and governance-related.

3. Automobiles & EV Ecosystem: ESG as Growth Strategy

What went well

EV adoption accelerated

Sustainability aligned with product innovation

Cleaner mobility positioned as future competitiveness

Visible examples

Tata Motors’ EV leadership

Mahindra & Mahindra’s EV platform investments

Maruti Suzuki’s gradual shift narrative

What needs improvement

Battery sourcing transparency

End-of-life recycling infrastructure

Supplier ESG readiness

ID lens takeaway

ESG worked best where sustainability directly shaped future revenue.

4. FMCG & Consumer Goods: Social Strength, Supply-Chain Risk

What went well

Strong water stewardship

Farmer engagement programs

Packaging innovation

Visible examples

ITC’s water positivity

Hindustan Unilever’s supplier programs

Nestlé India’s rural sourcing focus

What struggled

Traceability beyond Tier-1 suppliers

Contract labour vulnerabilities

Plastic waste management at scale

ID lens takeaway

FMCG ESG credibility depends less on factories—and more on thousands of invisible suppliers.

5. IT & Technology: Environmental Leadership, Social Stress

What went well

Carbon neutrality progress

Renewable energy adoption

Transparent ESG reporting

Visible examples

Infosys’ carbon-neutral disclosures

TCS and Wipro’s renewable sourcing

What cracked in 2025

Layoffs and workforce rationalisation

Burnout and attrition

Inconsistent handling of employee exits

ID lens takeaway

In services, ESG credibility is judged not by emissions—but by how people are treated in downturns.

Policies were common. Execution was uneven. Accountability made the difference.

Why This Matters for 2026

As India enters 2026, ESG maturity will no longer be judged sector by sector—but decision by decision.

The question will not be:

“Does this sector perform well on ESG?”

It will be:

“Does this board act responsibly when trade-offs are unavoidable?”

That answer will define the next phase of ESG in India.

7. Hope, Warning, and the Road to 2026

Despite the discomfort of 2025, there is genuine reason for optimism.

Boards now recognise ESG as a governance issue. Management understands that ESG leaves evidence. Investors increasingly reward substance over storytelling.

If 2025 exposed cracks, 2026 offers the opportunity to reinforce the foundation.

Not with louder commitments — but stronger systems. Not with perfect narratives — but honest disclosures. Not with fear — but accountability.

The warning is clear: ESG credibility will not survive comfort.

The hope is stronger: ESG integrity can still be rebuilt through discipline and courage.

Call to Action for 2026

For Boards & Independent Directors Ask harder questions. Demand evidence. Treat ESG risk like financial risk.

For Management Embed ESG into capital allocation, workforce decisions, and supply-chain governance.

For Investors Reward transparency. Interrogate execution. Use capital responsibly.

For ESG Professionals Choose integrity over optics. Build systems that withstand scrutiny. Speak up.

Conclusion: What 2026 Will Remember

ESG is not about image. It is about impact.

It is revealed when growth slows, costs rise, and decisions hurt.

2025 showed how ESG behaves under pressure.

2026 will decide whether lessons were learned.

Because ESG’s future in India will not be written in reports.

It will be written in choices — made quietly, and judged publicly.

SEBI reviewing ESG disclosure requirements for listed firms — shows evolving regulatory scrutiny and capacity challenges in reporting. Reuters

SEBI’s BRSR (Business Responsibility & Sustainability Reporting) has become mainstream reporting for top Indian companies (documented in various BRSR reports & manuals). ICSI

📊 Corporate ESG Actions & Performance

Automobile & Mobility Sector

Tata Motors partners with TCS for digital ESG reporting and sustainability tracking, embedding real-time data and compliance with SEBI’s BRSR. Tataworld+1

Tata Motors’ formal BRSR demonstrates environmental efforts including effluent processing and water recycling. Tata Motors

Brand & Sustainability Perceptions

Tata Group leads Indian brands in sustainability perception value, highlighting strong ESG positioning among Indian corporates. Brand Finance

IT & Technology Sector

Infosys outlines an updated ESG Vision 2030, including ongoing carbon neutrality and broader social/employment commitments. infosys.com

Manufacturing & Industrial Sector Recognition

Business Today “Most Sustainable Companies 2025” lists firms such as JSW Steel/JSW Energy, Mahindra & Mahindra, Hindustan Unilever, Godrej Properties for sustainability performance. Business Today

Climate & Energy Transition Initiatives

Indian corporates (e.g., L&T, Vedanta, RPG Group) expand sustainability programmes covering emissions, water, biodiversity and climate resilience. esgbroadcast.com

Trend & Commentary on ESG Reporting in India

Articles highlight that Indian companies are accelerating ESG initiatives as climate risks grow, but also face challenges in reporting quality and supplier data. esgbroadcast.com

Tech and automation (AI, blockchain, automation) are being explored to improve ESG data management and reporting quality in India. Times of India

Analyses suggest net-zero and Scope 3 reporting gaps remain in many Indian corporate disclosures — a reality check on the pace of transition. The Indian Express

ESG Illusion:A Company That Believed It Was Doing Everything Right

GreenGlow Energy had become a name synonymous with sustainability in India.

Listed on the NSE, operating across solar and wind assets, and frequently quoted in media as a “model renewable energy company”, GreenGlow’s leadership genuinely believed they were ahead of the curve. Their sustainability reports were polished, visual, and optimistic. Each year, they won awards. Each year, their ESG section grew thicker, glossier, more confident.

Inside the organisation, ESG was a source of pride.

Inside the boardroom, ESG was considered “handled.”

Until it wasn’t.

The London Roadshow: When Applause Turned into Silence

The investor roadshow in London was meant to be routine. Meetings with global funds, climate-focused investors, and ESG-themed portfolios were expected to reinforce GreenGlow’s premium positioning.

The presentation went smoothly—until the questions began.

One analyst flipped through the sustainability report slowly before looking up.

“You report under GRI. Can you also show us your SASB metrics—particularly how climate risks affect asset profitability?”

Another followed.

“Your report highlights 70% renewable energy usage. But there is no disclosure on Scope 3 emissions. Why?”

A third question cut deeper.

“MSCI rates you AA. Sustainalytics categorises you as High Risk due to governance concerns. Which rating reflects reality?”

The room grew quiet.

There was no hostility. No accusation.

Just a pause that felt uncomfortably long.

For the first time, GreenGlow’s leadership sensed something unsettling: their ESG story sounded strong—but did not feel investable.

The Emergency Board Meeting: Where ESG Became a Strategic Issue

Back in India, the board convened earlier than scheduled.

Some directors felt the investors were being unreasonable.

“We already report under GRI,” one executive argued. “It’s globally recognised. We win awards. Why complicate things?”

Others were uneasy.

The Independent Director, entrusted with protecting long-term shareholder interests, listened carefully. What was unfolding was not a reporting debate—it was a trust dilemma.

And the Independent Director framed it clearly for the board:

“This is not a debate about frameworks. This is a debate about credibility, capital, and regulatory readiness.”

The board was asked to step back—and look at the bigger picture.

Question 1: GRI or ISSB? The False Choice Boards Keep Making

Why GRI Felt Safe

GreenGlow’s comfort with GRI was understandable.

GRI had allowed the company to:

Showcase community impact

Highlight renewable achievements

Tell a compelling sustainability journey

GRI answers one powerful question:

How does the company impact the economy, society, and environment?

For stakeholders, NGOs, employees, and policymakers, this mattered deeply.

But the Independent Director reminded the board of an uncomfortable truth:

“Capital markets do not invest in intentions. They invest in risk-adjusted future cash flows.”

GRI, by design, is impact-focused, not financial-risk-focused.

Why Global Investors Were Asking for SASB, TCFD, and ISSB

The London investors were not rejecting sustainability. They were demanding decision-useful ESG information.

SASB answers: Which ESG issues financially matter for this specific industry?

TCFD answers: How does climate risk alter strategy, asset values, and resilience?

ISSB integrates ESG into the language investors already trust—financial reporting.

The Independent Director explained it plainly:

“GRI explains values. ISSB explains valuation.”

ISSB does not replace sustainability—it disciplines it.

The Regulatory Reality: Why BRSR Changes Everything

At this point, the board realised something critical had been missing from the discussion.

SEBI’s BRSR Core.

From the next financial year:

ESG disclosures would be mandatory

Key metrics would require assurance

Boards would be held accountable for accuracy

BRSR is not merely an Indian compliance document.

It quietly pushes companies toward:

Standardised metrics

Governance accountability

Financial materiality

In spirit, BRSR aligns far more with ISSB discipline than with pure GRI storytelling.

The Independent Director issued a clear warning:

“If we delay ISSB alignment, BRSR compliance will become a last-minute firefight—with reputational and regulatory risk.”

The Strategic Conclusion

The board was guided to a mature, non-binary decision:

GRI remains for stakeholder communication

ISSB becomes the backbone for investor, regulator, and lender trust

GRI would tell the story. ISSB would protect the balance sheet.

Question 2: The Credibility Gap Between Glossy Reports and Investor Reality

The board then confronted a harder question:

Why didn’t investors believe what they read?

The Independent Director identified three deep cracks beneath the surface.

1. Scope 3 Emissions: The Risk That Wasn’t Named

GreenGlow proudly disclosed Scope 1 and 2 emissions.

But Scope 3—supplier emissions, lifecycle impacts, logistics—accounted for 65% of its carbon footprint.

And it was missing.

The Independent Director explained the investor mindset:

“When a material risk is absent, analysts assume it is unmanaged—not immaterial.”

Best practice was not perfection.

Best practice was:

Screening-level estimates

Transparent assumptions

Clear boundaries

Silence, the board realised, was the most damaging disclosure of all.

2. Governance: ESG Without Ownership Is Theatre

ESG responsibility at GreenGlow sat across teams:

Sustainability prepared reports

Operations owned data

Risk teams stayed peripheral

No single board committee owned ESG risk.

The Independent Director was firm:

“If ESG is not owned at board level, it is not believed by the market.”

The recommendation:

A dedicated Board ESG & Risk Committee

ESG integrated into Enterprise Risk Management (ERM)

Climate and governance risks reviewed quarterly

This transformed ESG from narrative to oversight.

3. Assurance: The Difference Between Claims and Evidence

GreenGlow’s data was internally reviewed—but not independently assured.

Investors noticed.

The Independent Director reminded the board:

“In capital markets, unaudited ESG data is treated like unaudited financials—interesting, but not trusted.”

With BRSR Core mandating assurance, the path was clear:

Start with limited assurance

Move toward reasonable assurance

Align ESG controls with financial controls

Trust, the board learned, is built through verification—not vocabulary.

How Independent Directors Helped a Gig-Economy Unicorn Prepare for an IPO Without Losing Its Soul

Table of Contents

In early 2024, DriverU Mobility Services Ltd.—India’s fastest-growing on-demand driver platform—was a darling of the gig economy.

With ₹850 crore in FY23 revenue, 45,000 gig drivers, and 18-city operations, the company was sprinting toward an IPO planned just 18 months away.

But beneath its explosive 180% YoY growth, DriverU was sitting on a silent landmine:

It had zero ESG systems, zero sustainability reporting, and zero data for 98% of its workforce—because those 45,000 people were not “employees,” but gig workers.

And with investor pressure increasing, the company was about to learn that high growth does not protect anyone from ESG expectations.

Chapter 1: The Wake-Up Call in the Boardroom

The quarterly board meeting began with a sentence that froze the room.

“As a post-IPO top 1,000 listed company, you must publish full BRSR Core with assurance on Day 1,” announced Priya Deshpande, the independent director with 20+ years in sustainability.

CEO Raghav Jain was stunned.

“But we have no employees—only contractors! And we don’t even know what vehicles they drive. How do we report Scope 3?”

Priya leaned forward.

“That’s exactly why this is an existential risk. Gig economy companies don’t fit neatly into BRSR—but investors won’t accept that excuse.”

The board began evaluating the three strategic ESG approaches prepared by management.

Chapter 2: Three Paths — and One Realistic Future

Approach A — Compliance Minimum

Only report office emissions, tech team metrics, and exclude gig workers completely.

Priya shook her head.

“This will fail institutional investor expectations. PE investors already need ESG for exits. And regulators will not accept invisibilising 45,000 workers.”

Approach B — Industry-Leading Transparency

Treat gig drivers as value chain workers, collect full welfare and emissions data.

CFO objected: “Collecting that much data from 45,000 drivers is operationally impossible.”

Priya corrected him:

“No—it requires system redesign. Not impossible. Just uncomfortable.”

Approach C — Integrated GRI + BRSR

Use BRSR for compliance but integrate GRI topics to tell the full stakeholder story.

This was closest to reality.

After a heated debate, Priya summarized:

“Your reporting must be ambitious enough to satisfy investors, feasible enough to execute in 12 months, and transparent enough to build trust.”

Add fields: ✔ vehicle type ✔ fuel efficiency ✔ fuel used per trip ✔ earnings per hour ✔ break hours ✔ safety incidents

App auto-logs trip distance & idle time

Mandatory onboarding verification via RC upload

3. Establish Data Infrastructure

API connections similar to L&T’s ESG platform

Carbon accounting engine integrated like HDFC

Blockchain layer for income transparency

ML anomaly detection for driver-reported data

4. Prepare Range-Based Scope 3 Estimates

Estimate emissions where data unavailable (Maruti methodology)

Publish assumptions transparently

Begin pilot EV transition program

5. Begin First Assurance Preparations

Select assurance partner

Dry-run BRSR report

Gap analysis

🟩 Post-IPO: 12-Month Execution

1. Full BRSR Core + GRI Integrated Report

One report

One assurance

One dataset

2. Gig Worker Welfare Scorecard

Quarterly metrics sent to board:

median driver earnings/hour

% earning above city minimum wage

incident rates

% hours rested vs worked

driver satisfaction / grievance redressal time

women driver recruitment program

3. Scope 3 Emissions at Scale

45,000-driver vehicle data integrated

AI-based accuracy checks

Sample audits with telematics partners

EV transition incentives added to platform ranking

4. ESG Incentives in Leadership Pay

20% weighting based on: ✔ driver satisfaction ✔ grievance resolution ✔ safety ✔ emissions reduction

Priya insisted:

“Without linking compensation, ESG will remain a hobby—never a discipline.”

Chapter 3: The Data Revolution at DriverU

CTO Karan initially resisted the overhaul.

“Redesigning the app will delay our product roadmap.”

Priya countered:

“If your technology can match 45,000 drivers to 12 lakh trips a month, it can collect 10 ESG data points. This is the price of being a public company.”

The New System (Independent Director–Guided Design)

(a) Gig Worker Welfare Measurement

Collected automatically via app:

Verified earnings per hour

Real-time work hours

Rest periods

Corporate client tips & rating

Safety incident logs

Health insurance opt-in tracking

Validation:

Cross-checks with trip logs

anomaly detection for fake reporting

monthly sample audits

Blockchain:

Transparent earnings ledger

PE investors can verify payouts without accessing personal data

(b) Scope 3 Emissions Measurement

Data collected:

Vehicle type

year of manufacture

fuel efficiency

fuel consumed per trip

idle time

Model:

Hybrid actual + estimated model

City-based emission factors

6-monthly vehicle verification

Output:

“Range-based emissions disclosures”

Driver-level emission dashboard to nudge EV transition

(c) Social Impact Metrics

DriverU created a Mobility Impact Score:

emissions saved vs personal car ownership

% drivers crossing living wage

% women drivers

safety enhancement improvements

urban congestion reduction (AI-estimated)

Priya’s message to the board:

“This is how you justify your existence to society. Not just investors.”

Chapter 4: Winning Back Stakeholders

Priya crafted a stakeholder communication strategy that changed DriverU’s public perception.

Stakeholder Engagement Plan (Independent Director–Led)

1. PE & Institutional Investors

Concern: exit readiness, comparable ESG metrics, audited data Strategy:

Quarterly ESG investor deck

Assured BRSR + GRI integrated report

Transparent Scope 3 assumptions

Blockchain-based welfare data access

2. Gig Drivers

Concern: distrust, opaque earnings, lack of safety Strategy:

Driver App “My ESG Dashboard”

monthly earning transparency

grievance turnaround target: <48 hours

safety hotline

new program: Women on Wheels (1000 female drivers in Year 1)

A Story of How One Marketplace Almost Collapsed — and How It Fought Back

Table of Contents

ESG Compliance Crisis — When Growth Outruns Governance

For years, ShopKart, India’s fastest-growing e-commerce platform, was hailed as an unstoppable force. Venture capitalists celebrated its meteoric rise. New sellers joined in thousands every month. Customers loved the convenience, prices, and assortment. Revenue graphs pointed to the sky.

Every quarterly review was a victory lap. Every festival season outperformed the last. Every new city expansion looked like another step closer to IPO glory.

The internal dashboards showed a number that kept the company’s valuation soaring:

GMV — Gross Merchandise Value,

the total value of goods sold on the platform before cancellations, returns, or commissions.

ShopKart’s GMV had crossed ₹5,600 crore, signalling industry dominance and market trust.

But behind the rapid ascent lay a dangerous truth — ShopKart’s compliance systems hadn’t grown with it. No proper ESG controls. No systematic seller audits. No risk categorisation. No early-warning system.

Growth was accelerating faster than accountability — and a major crisis was brewing.

SECTION 1 — The Storm Arrives

Month 1 — A Story the Company Did Not Want to Face

An investigative nonprofit published a damning report revealing that 15% of ShopKart’s top handicraft sellers were sourcing from units employing child labour in rural clusters.

🔗 ESG Compliance and Supplier Risk Best Practices — This article explains how ESG compliance integrates environmental, social, and governance factors into supply chains, why non-compliant suppliers pose risks (reputational, operational, legal), and how technology and real-time monitoring help address those risks. ESG Compliance For Suppliers: Best Practices (fauree.com)

An ESG Case Study for Boards, Investors & Risk Leaders

Table of Contents

ESG Crises:THE DAY THE CALL CAME

On a warm Monday morning in Mumbai, the leadership of PharmaPlus, India’s second-largest generic drug manufacturer, began their week like any other. The company was riding high: ₹4,500 crore annual revenue, exports to 72 countries, and a spotless reputation cemented over 35 years.

But at 10:18 AM, an email arrived that would shake the company’s very core.

Subject: URGENT – FDA INSPECTION FINDINGS ON METAFLOX API

Three attached documents. One sentence in the body:

“Carcinogenic nitrosamine impurities detected. Supplier traced to PharmaPlus API source.”

The company’s world tilted.

By sunset, PharmaPlus’ share price had dropped 11%. That was just the beginning.

What no one in the company understood yet was this: This was not a contamination issue. This was a governance issue. And only one person saw that clearly — the Independent Director who had joined the Board just five months earlier.

THE FIVE-WEEK MELTDOWN

The story of PharmaPlus’ supply-chain collapse unfolded like a slow, painful movie.

Week 1: The U.S. FDA Bombshell

FDA traced carcinogenic impurities to a Chinese API supplier, Qingdao BioChem, a key provider for Metaflox, PharmaPlus’ best-selling diabetes medication.

Qingdao BioChem had passed its certification audit last year. PharmaPlus had trusted the certificate. And now 1.8 million patients were potentially exposed.

Week 2: EMA Drops the Hammer

The European Medicines Agency (EMA) suspended import licences for 14 PharmaPlus products until supply-chain integrity was proven.

Failure to comply meant: Immediate suspension of all US exports.

This could cripple the company for years.

The Independent Director stepped in to lead the design.

BUILDING PHARMAPLUS’ NEW SUPPLY CHAIN SYSTEM

Over the next eight weeks, PharmaPlus re-engineered its global supply chain — not from operations, but from risk, ESG, and governance principles.

The Independent Director outlined a three-part framework that would redefine PharmaPlus forever.

A. Categorizing All 190 API Suppliers by Real Risk

A total of 190 suppliers were sorted not by geography not by volume not by comfort but by risk categories.

Category A – High Risk (28 suppliers)

Critical APIs

High impurity potential

Weak environmental oversight

History of deviations

Incomplete batch traceability

Category B – Medium Risk (62 suppliers)

Mid-volume APIs

Moderate ESG maturity

Partial digital systems

Category C – Low Risk (100 suppliers)

Strong QMS

Good ESG records

Based in EU/US/Japan/India

Transparent and digitally compliant

This was the first time anyone in the company had seen the system this clearly.

B. Audit Frequencies — Finally, Risk-Based

The Independent Director insisted:

“Audits should be proportional to risk, not convenience.”

A new schedule was implemented:

Category

Audit Type

Frequency

Additional Controls

A – High Risk

Full forensic ESG + GMP

Twice yearly

100% batch impurity profiling

B – Medium

Hybrid audits

Every 18 months

Quarterly document review

C – Low

Desktop audits

Every 2–3 years

Annual self-certification

Executives protested the cost. The Independent Director replied:

“Quality is expensive. But not as expensive as negligence.”

Silence again. Agreement followed.

C. Technology: The New Nervous System of PharmaPlus

Under the Independent Director’s guidance, PharmaPlus deployed an entirely new wave of digital infrastructure.

1. AI-Powered Supplier Risk Dashboard

Live integrations providing:

FDA/EMA/WHO alerts

COA deviations

ESG violation reports

Wastewater data

Worker safety incidents

Batch inconsistencies

For the first time, the Board had real-time visibility.

2. Blockchain Batch Traceability

Required under new EU regulations. Tracked API identity from raw material → reactor → batch → dispatch → final formulation.

3. IoT Environmental Monitoring

Sensors placed at Tier-1 suppliers:

pH

COD/BOD

VOC emissions

Effluent discharge metrics

Alerts were auto-escalated to QA leadership.

4. Digital Due Diligence Repository

All supplier CAPAs, audits, improvement logs, and certifications were uploaded, time-stamped, and monitored.

PharmaPlus had never been this transparent — even internally.

THE STRATEGY CROSSROAD — 3 ROADS, 1 FUTURE

At the next board meeting, the CFO presented three stark choices:

OPTION A: EXIT HIGH-RISK SUPPLIERS

Buy only from EU/US suppliers. Cost increase: ₹240 crore annually.

Independent Director’s Analysis:

Looks clean, feels safe

But it’s punitive

Damages MSME suppliers

Creates supply concentration risk

Increases cost of essential medicines

Violates ESG principles of shared progress

Verdict: Reject.

OPTION B: Build the strongest monitoring & capability ecosystem in the industry

Investment: ₹130 crore.

Independent Director’s Analysis:

Sustainable

Future-ready for EU 2026 rules

Builds long-term resilience

Reduces recurring risk

Strengthens all 190 suppliers

Aligns with “Collaboration over Punishment” philosophy

Mirrors the Unilever model: lift your ecosystem.

Verdict: Adopt.

OPTION C: Acquire 2–3 critical API suppliers

Investment: ₹900 crore.

Independent Director’s Analysis:

Great for strategic control

Reduces dependency

But capital-heavy

Operational integration risks

Useful but incomplete

Verdict: Selective adoption (only for critical APIs).

THE INDEPENDENT DIRECTOR’S FINAL RECOMMENDATION

The Board turned to him.

He spoke with clarity:

“We cannot escape risk. We must learn to govern it. The future is not in rejecting suppliers but in elevating them.”

His final recommendation:

Adopt Option B as the core strategy

Supplement with Option C for 2–3 mission-critical API suppliers

Reject Option A completely

The Board voted. Unanimous.

A transformation had begun.

HOW PHARMAPLUS EARNED BACK TRUST

Trust is rebuilt slowly. Carefully. Patiently.

But over the next 18 months, PharmaPlus did just that.

1. Regulators Took Notice

FDA acknowledged the strength of the Supply Chain Integrity Plan. EMA reinstated licences after 4 months.

2. Investors Returned

The same institutional investors who wrote angry letters wrote a different one later:

“PharmaPlus is now a global benchmark for supply-chain governance.”

Share prices stabilized, then rose 17%.

3. Suppliers Became Partners

Small, MSME API vendors in India and China received:

ESG training

Emissions-control guidance

Quality system upgrades

Wastewater management support

PharmaPlus built a new ecosystem — not by firing suppliers, but by uplifting them.

4. The Company Culture Shifted

Employees understood ESG not as compliance but as identity. Operators reported early deviations. Quality teams enforced stricter controls. Procurement aligned with sustainability, not price.

5. Patients Regained Confidence

When the new “TraceMyMedicine” QR system launched, patients could scan any PharmaPlus pack to see full traceability. This transparency became a competitive advantage.

THE NEW PHARMAPLUS — STRONGER AFTER CRISIS

Two years after the meltdown, PharmaPlus had become:

India’s most transparent pharma supply chain

One of Asia’s first companies with end-to-end blockchain traceability

A global case study for ESG-driven risk governance

A trusted partner of FDA, EMA, and CDSCO

A brand stronger than ever before

The Chairman called it:

“The greatest crisis in our history, and the greatest transformation we ever achieved.”

But everyone on the Board knew one truth:

It started with the courage of one Independent Director who refused to accept the word “isolated.”

FINAL REFLECTION: THE LESSON FOR THE WORLD

PharmaPlus’ story is not unique.

Across the world, pharma supply chains are cracking under:

weak oversight

fragmented suppliers

cost pressure

ESG violations

global regulatory demands

rising patient expectations

The lesson from PharmaPlus is clear:

Quality is not born in laboratories. Quality is born in supply chains.

A company is only as ethical as its lowest-tier supplier. A brand is only as strong as its weakest oversight mechanism. And a Board is only as competent as its governance of risk.

PharmaPlus nearly fell apart. But it rose again — because someone finally asked the right questions.

It was one of those late evenings in Mumbai when the monsoon taps loudly on the windows—like the sky itself reminding you that nature doesn’t wait for board approvals.

Inside the polished glass walls of Suryanet Global, an Indian multinational with operations in IT, pharma, and metals, the atmosphere was impossibly tense.

Three business heads sat in front of the CEO, looking both tired and overwhelmed.

Shalini, head of sustainability, broke the silence:

“Everyone is asking us to report something different. Investors want SASB. Regulators want BRSR. Clients ask for GRI. Europe insists on CSRD. Climate funds demand TCFD. We’re drowning.”

The CFO added nervously:

“Our teams are burning out. We keep producing reports, but I’m not sure we understand what actually matters to our business.”

And then the CEO—Vikram Sharma—asked the question that changed everything:

“Forget the noise. Which frameworks truly matter for us—and why?”

This is the story of how one company found clarity in the storm. A story of courage, discernment, and choosing meaning over compliance.

This is the story that every Indian company—every board, CEO, and CHRO—needs to hear.

1. The Night the CFO Found SASB—and Found His Focus

Two months earlier, Vikram had returned from an investor roadshow where a US fund manager bluntly told him:

“I don’t care about your 120-page sustainability report. Show me the 5 things that actually impact your margins, growth, and risks.”

Vikram didn’t have an answer. So that night, he stayed back in his office and opened the SASB website. Within minutes, he felt something shift inside him.

Here, finally, was a framework that cut the clutter.

**SASB wasn’t asking companies to report everything.

SASB asked companies to report only what truly matters financially.**

It wasn’t philosophical. It wasn’t moralistic. It was surgical.

And for the first time, Vikram saw a path through the chaos.

2. SASB: The Framework That Speaks the Language of Business

Shalini explained it to the board beautifully:

“SASB speaks the language investors understand—risk, returns, margins, growth.”

SASB doesn’t dump generic ESG topics onto companies. It carefully identifies the 3–7 ESG issues that matter most for financial performance in each industry.

The brilliance? It’s empirical—not ideological.

It studies patterns across thousands of companies to find which ESG issues move:

✔ revenue ✔ cost of capital ✔ operational efficiency ✔ legal liabilities ✔ supply chain resilience

This meant clarity. Precision. Focus.

Let’s revisit the framework through Suryanet’s three sectors.

💻 For IT Services (like Suryanet’s Digital Division): SASB focuses on 5 issues

1. Data security & customer privacy

Because one breach can erase decades of trust.

2. Talent recruitment & retention

Because people are the business.

3. Competitive behavior & IP protection

Because innovation is fragile.

4. Systemic tech disruptions

Because outages can cost millions per hour.

5. Energy use in data centers

Because clients now choose vendors based on carbon footprint.

Vikram whispered to Shalini:

“This is exactly what our investors ask us about.”

💊 For Pharmaceutical Companies (like Suryanet Pharma): SASB sharpens focus

1. Product quality & safety

If drugs fail, nothing else matters.

2. Clinical trial management

Because ethics is existential.

3. Access to medicines & pricing

Because reputations are fragile.

4. Employee safety

Because labs & plants carry real hazards.

5. Legal & regulatory risks

Because non-compliance destroys credibility.

The pharma CEO sighed:

“We’ve been reporting everything except the five things that could actually shut us down.”

🛠 For Steel Companies (like Suryanet Metals): SASB brings hard truths

1. Greenhouse gas emissions

Because decarbonization is not optional anymore.

2. Air quality & compliance

Because regulatory penalties can cripple operations.

3. Water & wastewater management

Because steel depends on water availability.

4. Waste & hazardous materials

Because circularity is competitive advantage.

5. Workforce health & safety

Because safety failures are reputation killers.

The head of Metals spoke quietly:

“This is finally something we can act on.”

3. The Indian Reality: When SEBI’s BRSR Becomes a Mirror

Just when the board began celebrating SASB clarity, Shalini reminded them gently:

“SASB gives us financial relevance. But SEBI’s BRSR gives us Indian relevance.”

This wasn’t reporting. This was corporate introspection.

**BRSR asks:

What does India expect from you? How does your company impact the real world?**

It forces companies to reflect on:

✔ local hiring ✔ community health ✔ water usage in drought-prone regions ✔ labour practices in supply chains ✔ biodiversity around industrial areas ✔ CSR impacts ✔ employee well-being

For the first time, the board saw:

SASB shows what matters financially. BRSR shows what matters socially.

And both were essential.

4. GRI: The Framework That Looks Into the Soul of a Company

A week later, Suryanet hosted a townhall with 2,800 employees across India.

A young engineer from Pune asked:

“We talk so much about our business goals. When will we talk about our societal goals?”

And that day, the leadership understood what GRI truly is.

GRI is not about the company’s finances. GRI is about its footprint on people, planet, and society.

It asks:

How do your decisions affect communities?

How do your operations affect biodiversity?

How do your policies affect workers, women, suppliers?

How do you impact the economy?

How do you protect vulnerable groups?

GRI forces companies to think deeply, morally, humanly.

**The result?

A 360-degree view of materiality. A mirror that reflects all impacts.**

But yes—GRI can become overwhelming. Lists can stretch endlessly unless leaders have discipline.

And that was the turning point.

5. The Moment the CEO Realized: “We Don’t Have to Choose One.”

Vikram called another meeting and said:

“Why are we treating frameworks like competitors? They are not rivals. They are tools.”

And then he laid out the idea that transformed Suryanet forever.

6. The Integrated Approach: The Map That Changed Everything

The leadership aligned on a simple but brilliant strategy:

⭐ Use the strengths of each framework instead of choosing one.

1. Use SASB for financial relevance

→ Focus on what drives profit, risk, and competitive advantage.

2. Use GRI for societal relevance

→ Understand how the company impacts people and the planet.

3. Use BRSR for Indian relevance

→ Meet SEBI rules and address local expectations.

4. Use TCFD for climate relevance

→ Integrate climate risk into strategy and capital planning.

5. Use TNFD for nature relevance

→ Understand dependencies on biodiversity, water, ecosystems.

Together, these frameworks created something powerful:

A complete, holistic, authentic understanding of what matters.

Not reporting for the sake of reporting. Reporting that drives strategy. Reporting that drives resilience. Reporting that builds trust.

7. TCFD: The Day Climate Risks Became Hard Numbers

A climate consultant presented two scenarios:

A 2°C world

A 4°C world

The CFO watched in disbelief as the models revealed:

Raw material volatility under extreme heat

Rising insurance premiums

Disruption of chemical supply chains

Water scarcity risks

Client requirements for decarbonization

For the first time, climate change was not abstract. It had rupee values.

TCFD became the bridge between climate science and financial planning.

TNFD: When the Steel Plant Manager Broke Down

During a site visit in Jharkhand, a steel plant manager pulled Vikram aside.

In a trembling voice, he said:

“Sir, the local river we depend on is shrinking every year. We never included nature risk in our planning. If this river fades, our plant will die.”

That day, TNFD stopped being a “future framework.” It became a survival framework.

It asked:

What ecosystems do we depend on?

How vulnerable are they?

What risks emerge from biodiversity loss?

What opportunities arise from restoring nature?

TNFD became the heart of the company’s long-term resilience planning.

8.ISSB: How It Evolved — The Full Story

The International Sustainability Standards Board (ISSB) did not appear overnight.

It is the result of a 10-year global convergence journey—bringing together many fragmented ESG frameworks into one global baseline for sustainability disclosures.

Below is the simplest and most accurate evolution timeline.

✅ Step 1: The Origins — Three Major Frameworks Start the Movement

1. SASB (2011) — Industry-specific metrics

Established in the U.S.

Focused on financially material ESG issues by industry.

Created 77 industry standards.

Used widely by investors (especially in U.S. capital markets).

2. TCFD (2015) — Climate risk reporting

Created by the Financial Stability Board (FSB).

Focused on:

Climate risks & opportunities

Scenario analysis

Governance

Strategy

Metrics & targets

Became the global benchmark for climate disclosures.

3. Integrated Reporting Framework (IR) (2013)

From the International Integrated Reporting Council (IIRC).

Emphasized connected reporting: how strategy, governance, and performance create long-term value.

These three set the foundation.

✅ Step 2: The Big Consolidation (2020–2022)

By 2020, companies complained that sustainability reporting was confusing and fragmented.

ISSB evolved from the consolidation of SASB, IIRC, CDSB, and the adoption of TCFD principles, forming a single, global sustainability reporting baseline under the IFRS Foundation.

9. The Final Breakthrough: A Framework Isn’t a Report—It’s a Lens

By the end of the year, Suryanet didn’t just “comply” with frameworks.

They used them to:

rewrite their business strategy,

redesign their risk processes,

reorganize their leadership structure,

rethink their community partnerships,

redefine their purpose.

Frameworks finally became what they were always meant to be:

Not burdens. Not obligations. But lenses that help leaders see clearly.

Global Frameworks (Standards & Voluntary Bodies)

Framework

Focus

Materiality

Mandatory in 2025?

Relevance in 2025

Key Strength

Key Limitation

SASB

Industry-specific financially material ESG issues

Financial

Partially mandatory (via ISSB when adopted by regulators)

Not mandatory yet (expected 2026–2027 in some regions)

High & rising — major for agri, mining, FMCG, infra

Strong nature risk framework

Complex, still maturing

ISSB (IFRS S1 & S2)

Global baseline for sustainability & climate

Financial

Mandatory or being adopted by 25+ countries incl. UK, Australia, Singapore, Canada (phased)

Extremely High — de facto global standard

Globally consistent, investor grade

Limited social topics

BRSR (India – SEBI)

Indian ESG disclosure rule

Financial + Impact

Mandatory for top 1,000 Indian listed companies

Extremely High – India’s core reporting rule

Context-specific, stakeholder focused

Quality varies, evolving

🚩Quick “Red-Flag / Must-Know” Summary for 2025 Boards

Framework

Mandatory in 2025?

Why It Matters for Boards

SASB

Indirectly (through ISSB adoption worldwide)

Industry KPIs investors demand

GRI

Indirectly mandatory in EU

Needed for stakeholder impact reporting

TCFD

Mandatory in many markets & absorbed into ISSB

Still the backbone of climate disclosure

TNFD

Not mandatory yet, but expected soon

Nature impact is becoming the “next climate”

ISSB

Mandatory in 25+ countries by 2025–26

Emerging global baseline. Key for future compliance

BRSR (India)

Mandatory NOW

Core requirement for Indian listed companies

EU CSRD

Mandatory

Toughest overhaul of sustainability reporting

US SEC

Mandatory climate reporting

Applies to all US-listed Indian multinationals

UK SDR / Australia / Singapore / Japan

Mandatory

ISSB becoming global reporting language

2025 Relevance Ranking (Most to Least Impactful)

1. ISSB (global baseline — investor required)

2. CSRD/ESRS (most comprehensive & mandatory)

3. TCFD (still required + core of ISSB)

4. SASB (industry metrics used everywhere)

5. BRSR (India-specific, mandatory)

6. GRI (stakeholder expectations, EU alignment)

7. TNFD (emerging, will grow fast post-2026)

10. The CEO’s Note That Every Leader Should Read

Vikram’s message to the entire company became iconic. It was printed at the entrance of the corporate office.

“SASB taught us what drives our business. GRI taught us what drives our impact. BRSR taught us what drives our India story. TCFD taught us what drives our resilience. TNFD taught us what drives our survival.

ISSB integrates ESG with IFRS -Financials Together, these frameworks taught us who we truly are.”

11. And Finally: The Question Every Company Must Answer

After a year of learning, unlearning, and integrating, the leadership asked itself one powerful question:

“What is truly material for us?”

Not because regulators demanded it. Not because investors pressured it. Not because clients expected it.

But because they wanted their company to operate with:

clarity

purpose

responsibility

resilience

pride

And the answer became their North Star.

✨ Final Takeaway: Don’t Fear the Frameworks—Use Them to Find Yourself

SASB shows you what affects your financial performance. GRI shows you how you affect the world. BRSR shows you what India expects from you. TCFD shows you how climate change reshapes your future. TNFD shows you why nature is your greatest asset.

ISSB applies IFRS-style standards to ESG issues so companies report sustainability with the same confidence as financials.

You don’t have to choose one. You only have to choose clarity.

Frameworks are not complexity. Frameworks are wisdom, dressed as compliance.

And once you understand how to use them— your business stops surviving and starts transforming.

A factory worker whispers: “There are cracks in the wall. We shouldn’t go in today.”

A customer whispers: “Something feels off. They just don’t care like before.”

And somewhere in a glass boardroom — surrounded by dashboards, charts, and KPIs — those whispers get drowned by ambition.

“Later.” “We can push harder.” “We need to hit the quarter.” “It’s manageable.”

But then, one day, the whispers become a scream.

Flights are cancelled by the thousands. Planes crash. Workers strike. Customers revolt. Scandals explode. Entire factories collapse. Brands burn down overnight.

Not because markets collapsed. Not because technology failed. Not because competitors won.

But because the company forgot its people.

This is the story of those collapses — IndiGo, Boeing, Uber, Amazon, Foxconn, Wells Fargo, Rana Plaza, OYO — not as accusations, but as lessons. Not to shame, but to warn. Not to judge, but to prevent future tragedies.

Because every corporate disaster is a human disaster first.

When the “S” in ESG fails, everything else follows.

1. IndiGo Crisis (2025): A People Problem That Became a National Breakdown

India witnessed scenes normally reserved for Hollywood disaster films — airport floors filled with stranded passengers, crying children, people sleeping on luggage, and thousands scrambling to reach weddings, interviews, exams, and funerals.

Why?

Not due to a natural disaster. Not due to a terror threat. Not due to a global emergency.

But because of crew fatigue, overloaded rosters, and lack of preparedness for updated rest and safety norms — all linked directly to the “S” pillar of ESG.

The Hidden Problem: People Were Exhausted

Reports highlighted:

Pilots operating on stretched rosters

Airline maintaining fewer pilots per aircraft than needed

Months of warnings about fatigue

Poor contingency planning for regulatory changes

Internal allegations of unrealistic workloads

When new safety norms kicked in, IndiGo didn’t have enough rested crew to fly.

The result?

A national aviation crisis.

The Human Cost

Families missed life events. Students missed exams. Elderly passengers slept on the floor. Airport staff took the anger. Pilots battled burnout.

Efficiency alone cannot keep a system running when its people are on the edge.

IndiGo’s crisis is a case study in how ignoring the Social pillar can cripple operations overnight.

2. Boeing 737 MAX: The Deadliest ESG-Social Failure in Modern Corporate History

Two crashes. Two aircraft full of families who never reached home. 346 lives lost. One of the greatest reputational and financial hits in aviation history.

The cause?

Internal warnings ignored. Safety concerns overshadowed by pressure to compete with Airbus. Pilots not adequately trained on new software. A culture that prioritised speed and market dominance over human safety.

This is the darkest example of what happens when profit outvotes people.

The human cost was irreversible. The corporate cost was billions.

3. Amazon Warehouses: When Human Bodies Meet Brutal Efficiency

Amazon is one of the most admired companies on earth. Yet its warehouses have faced global scrutiny:

Injury rates reportedly higher than industry averages

Workers rushing to meet algorithm-driven targets

Bathroom breaks timed

High turnover

Allegations of dehumanising conditions

Amazon has since invested heavily in safety improvements — but the early years showed what happens when hyper-efficiency forgets human capacity.

You can build the world’s fastest logistics machine. But not on exhausted backs forever.

4. Uber: A Culture That Grew Too Fast, Until It Collapsed Inward

Uber wasn’t destroyed by competitors. It was wounded by its own culture.

Reports described:

Widespread harassment

Managerial bullying

Retaliation fears

Grey-area ethics

A “bro culture” celebrated internally but condemned globally

The result?

CEO resignation

Massive valuation hit

Investor revolt

Global investigations

Reputation rebuild costing years

Uber’s story teaches one painful truth: No innovation survives a broken culture.

5. Foxconn & Apple: Workers Under Pressure in the World’s Most Efficient Factories

Foxconn, a key Apple supplier, faced global outrage after:

Long work hours

Dormitory-style living

Labour pressure

Multiple suicides at facilities

Apple intervened, audits were conducted, and conditions improved — but the episode revealed a global blind spot:

Efficiency is not sustainability. Human dignity is not optional.

6. Wells Fargo: When Internal Pressure Destroys Integrity

Wells Fargo employees were pushed to meet aggressive sales targets.

So aggressive that thousands resorted to creating millions of fake customer accounts without consent.

Why?

Because the internal pressure was crushing. And when people break, ethics break.

The consequences:

CEO resignation

Billions in fines

Regulatory restrictions

Severe reputational damage

This wasn’t a finance scandal. It was a social systems failure.

7. Rana Plaza: The Corporate Negligence That Took 1,100 Lives

Nothing reveals the true meaning of “Social” in ESG more painfully than Rana Plaza — a garment factory building in Bangladesh.

Workers saw cracks in the walls. They begged not to enter.

Managers forced them.

The building collapsed. 1,134 workers died. Thousands were injured. Families shattered forever.

This tragedy changed global supply chain standards — but at a cost too high to forgive.

It became the world’s loudest warning that ignoring workers is fatal.

8. OYO Rooms: Blitzscaling Beyond People Limits

As OYO scaled globally:

Small hotel partners complained about contract terms

Employees described burnout

Quality scores dropped

Lawsuits piled up

Global partners withdrew

The company stabilised later, but the lesson was clear:

Growth without people foundations collapses under its own speed.

THE PATTERN IS ALWAYS THE SAME

Across industries, countries, and decades, the same formula repeats:

When pressure grows and people weaken and leadership ignores and early warnings are silenced and culture turns fragile— the collapse begins.

Companies don’t fall because the market turns. They fall because their people do.

Why This Matters to Every Leader Today

Whether you run:

A conglomerate

A fintech

A renewable energy firm

A hospital chain

A logistics empire

An airline

A manufacturing unit

A consulting firm

… your survival depends on ONE thing:

How well you protect your people.

Not your revenue, not your brand, not your technology.

Because when fatigue meets silence, when ethics meet pressure, when customers feel invisible, when workers feel replaceable, and when safety becomes negotiable—

the countdown to collapse begins.

ESG Isn’t About Compliance. It’s About Humanity.

The Environmental pillar can be measured. The Governance pillar can be documented.

But the Social pillar must be lived:

Safety

Workload

Fairness

Dignity

Customers

Labour practices

Culture

Well-being

Transparency

Respect

Companies fail here because S is the hardest — and the most important.

The future will belong to companies that lead with empathy, not ego. Responsibility, not just revenue. Humanity, not just efficiency.

Because machines may run your operations, but people run your company.

FINAL MESSAGE: When People Rise, Companies Rise. When People Fall, Companies Fall.

IndiGo’s cancellations, Boeing’s crashes, Amazon’s fatigue complaints, Uber’s culture crisis, Foxconn’s suicides, Wells Fargo’s ethics collapse, Rana Plaza’s tragedy, OYO’s burnout — every story says the same thing:

Ignoring the “S” in ESG is not an oversight. It is a disaster waiting to happen.

And companies that listen to early whispers avoid the screams.

✨ Call To Action

Build a People-First ESG System Before the Next Crisis Hits

If you are a leader, board member, CXO, sustainability professional or investor, the most important action you can take now is:

👉 Create a robust, people-centric ESG-S framework that protects workers, customers, and the company itself.

A practical, story-driven guide with real-world examples

Table of Contents

In today’s fast-changing world, companies are under unprecedented pressure—from regulators, investors, customers, employees, and even the planet—to act responsibly and transparently. But the challenge is real:

How do you decide which ESG issues truly matter? Which ones deserve board attention? And how do you manage stakeholders with conflicting priorities?

This is where materiality assessment and stakeholder engagement become the strategic backbone of ESG leadership.

Let’s explore them through stories, real-world examples, and lessons from companies that got it right—and those that paid the price for ignoring them.

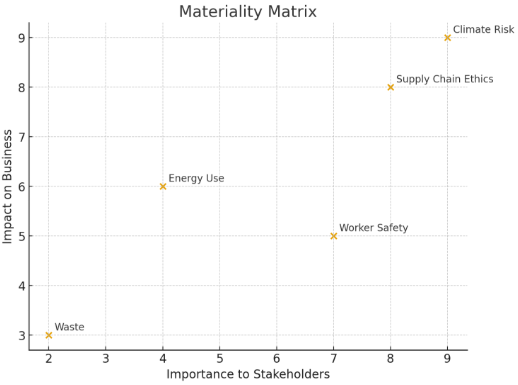

1. What Is Materiality? The Art of Choosing What Really Matters

Materiality is about identifying the ESG issues that can significantly impact a company’s financial performance and/or create substantial impact on stakeholders.

Think of it as corporate triage: What could truly make or break your business?

Most companies face dozens of ESG issues—climate, labor, waste, cybersecurity, human rights, diversity, water, supply chain ethics. But only some are material, meaning:

They influence long-term value creation

They affect critical stakeholder groups

They pose strategic, reputational, or regulatory risk

A robust materiality assessment cuts through the noise.

2. Why Materiality Matters: Lessons From the Real World

Volkswagen Emissions Scandal — Ignoring a Material Issue

VW treated emissions compliance as a technical issue, not a material governance risk. Outcome?

€30 billion in fines

Years of reputational damage

Loss of investor trust

Materiality blind spot: Ethics of engineering & transparent reporting.

Tesla’s Labor Relations Blind Spot

Tesla focused heavily on innovation and safety but underestimated labor issues—union tensions, worker fatigue, injuries.

Materiality blind spot: Workforce welfare.

Lesson: Social issues can become as financially material as environmental ones.

Wells Fargo — Culture Is Material

The bank ignored its toxic sales culture until it became a multi-billion-dollar crisis.

Materiality blind spot: Employee incentives, ethics, and governance.

Lesson: Internal culture is not “soft”—it can bankrupt trust.

Ørsted — Materiality as a Strategic Weapon

Once a fossil-heavy energy company, Ørsted used materiality to pivot toward offshore wind.

Do regulators, customers, communities, employees, or investors deeply care?

Example: In the auto sector, battery safety, supply chain ethics, and worker reskilling sit in the top-right quadrant—high business impact, high stakeholder interest.

That’s where board focus is needed.

4. Double Materiality: When Impact Matters as Much as Financials

Europe’s CSRD introduced the concept of double materiality:

Financial Materiality: Could this ESG issue affect the company’s value?

Impact Materiality: Could the company’s actions harm society or the environment?

Example: For a beverage company in India, water scarcity is both:

Financial risk (plant shutdowns)

Social risk (community protests, environmental impact)

But in Norway, with abundant water, the materiality changes.

5. Stakeholder Engagement: Turning Friction into Strategy

Identifying what matters is only half the battle. The real challenge: Stakeholders rarely agree.

Different stakeholders = Different concerns = Conflicting priorities.

A mature company maps them using a Power–Interest Grid:

High power, high interest: Regulators, governments, major investors

High power, low interest: Large institutional shareholders

Low power, high interest: Communities, NGOs, employees

High influence groups: Media, civil society, activists

Each group sees risk differently.

6. Real-World Stakeholder Conflict Examples

1. Apple & Supplier Labor Practices (China)

Stakeholders involved:

Workers (interest in conditions)

NGOs (interest in human rights)

U.S. government (power due to geopolitical tension)

Investors (concerned about brand risk)