Table of Contents

📱 India’s Digital Payment Story: From Cash to a QR Code

It’s 2016. You’re at a busy chai stall in Mumbai. The tea vendor pulls out a small cardboard with a black-and-white QR code. Instead of digging for coins, you take out your phone, scan, and—ping!—the payment is done in seconds.

Fast-forward to today: the same story repeats in villages, metros, malls, and even abroad. From a ₹10 chai to a ₹10,000 shopping spree, Indians are paying with UPI (Unified Payments Interface)—a system that has turned the country into the world’s #1 digital payments market.

But how did India make this leap when even the US and Europe still juggle cards, wallets, and fees? The secret lies in the technology and design of UPI.

The Rise of UPI

- Launched in 2016 by NPCI, UPI was designed as a seamless way to send and receive money instantly via mobile phones.

- Zero MDR (Merchant Discount Rate) initially attracted millions of merchants to accept payments.

- Today, UPI processes 15+ billion transactions monthly (2025 data expected to cross this mark).

- It works across apps (PhonePe, Google Pay, Paytm, BHIM, WhatsApp Pay) – making it interoperable and universal.

📅 Timeline of UPI

- 2008 – NPCI formed.

- 2010 – IMPS launched (precursor to UPI).

- 2012 – Aadhaar-enabled payments, RuPay card launched.

- April 2016 – UPI launched with 21 banks.

- 2017 – BHIM app released; Google Tez (later GPay), PhonePe enter.

- 2018 – QR acceptance explodes across small vendors.

- 2019 – 1 billion monthly UPI transactions.

- 2020 – COVID accelerates adoption; WhatsApp Pay enters.

- 2021 – UPI crosses 4 billion monthly transactions.

- 2022 – UPI Lite, Credit on UPI introduced; International expansion begins.

- 2023 – UPI crosses 10 billion monthly transactions.

- 2024 – UPI linked with Singapore PayNow, UAE, Mauritius, France.

- 2025 – India becomes #1 digital transactions market globally, projected 15+ billion monthly UPI payments.

📊 India – World’s Largest Digital Transactions Market

- In 2023, India processed 46% of the world’s real-time digital payments (per ACI Worldwide report).

- UPI clocked 100+ billion transactions in 2023 alone.

- China follows but mostly via private wallets (WeChat/Alipay), not bank-led universal infrastructure.

- US, UK lag in adoption due to lack of a single interoperable standard.

👉 This means: India is not just leading, it’s setting the model for the world.

Why UPI Clicked in India

- Simplicity – Just scan a QR code, enter PIN, and you’re done.

- Interoperability – One QR works across apps and banks.

- Trust & Government Push – RBI & NPCI ensured strong backend security.

- Financial Inclusion – Even small vendors and rural users got digital access.

- Cost Advantage – No charges for customers, minimal friction for merchants.

Impact on Economy & Society

- Cashless Push – Reduced dependence on cash, better transparency.

- Boost to SMEs – Street vendors, kirana shops, cab drivers went digital overnight.

- Women Empowerment – Easy money transfer helped women access financial independence.

- Data-led Credit Access – Digital footprints enabling micro-credit and BNPL models.

⚙️ The Technology Behind UPI

UPI is not “just an app”—it’s an open digital rail built by NPCI (National Payments Corporation of India). Think of it as an email system for money—free, instant, universal, and secure.

Here’s how it works in simple terms:

🔑 1. Virtual Payment Address (VPA) /UPI ID

Instead of remembering account numbers or IFSC codes, UPI uses a simple ID like an email (yourname@bank). This acts as your digital identity.

A UPI ID (also called Virtual Payment Address / VPA) is like an email address for money transfers. It’s a unique identifier that replaces the need to share sensitive bank details such as account number, IFSC code, or branch.

🔄 2. Real-Time Fund Transfer

When you pay, UPI connects directly to your bank account via the IMPS (Immediate Payment Service) infrastructure, ensuring 24×7, real-time settlement.

🛡️ 3. Multi-Layer Security

- Mobile number is linked to your bank account.

- Device binding ensures payments only from your registered phone.

- Two-factor authentication: UPI PIN + phone SIM validation.

🔗 4. Interoperability Across Banks & Apps

Unlike wallets (Paytm wallet, Venmo, WeChat Pay), UPI is bank-to-bank and app-agnostic. A QR code from SBI works if you use Google Pay, PhonePe, Paytm, or BHIM.

⚡ 5. API-Driven Innovation

NPCI built UPI on open APIs, so fintech apps can plug in without building their own rails. This is why competition (GPay, PhonePe, Paytm, Amazon Pay) thrives on a common backbone.

🌍 Why Other Countries Still Don’t Have Their Own UPI

In 2016, when India quietly launched UPI, few imagined it would grow into the world’s most successful digital payments system. Today, rickshaw drivers in Delhi, street vendors in Chennai, and luxury malls in Mumbai all accept a simple QR code scan. India now processes billions of transactions every month, leaving even advanced economies like the US, UK, and Europe wondering: “Why can’t we build something like this?”

The answer lies not just in technology, but in ecosystem, regulation, and vision. UPI was born from India’s unique blend of government-backed infrastructure (NPCI), interoperability across banks, and a push for financial inclusion. In contrast, most other countries are still fragmented—stuck between banks, card networks, and private payment apps competing for dominance.

UPI is not just an app, it’s a shared digital public good—something the world’s most developed economies never truly prioritized. And that is why, even in 2025, India stands alone with a seamless, real-time, and universal digital payment system.

Below we summarize key factors.

1. Fragmented Banking Systems

- In countries like the US or EU, each bank or card network has its own payment system.

- UPI succeeded because NPCI created a common protocol connecting all Indian banks under one roof.

- In contrast, banks in other countries compete instead of collaborating on a shared real-time platform.

2. Strong Card Network Dominance

- In developed countries, Visa, Mastercard, and PayPal dominate digital payments.

- These companies earn fees from merchants and resist zero-cost models like UPI.

- India skipped the “credit card era” and moved straight from cash → mobile → UPI, avoiding this bottleneck.

3. Regulatory Challenges

- India’s RBI and Government pushed banks to adopt UPI as mandatory infrastructure.

- In the US or Europe, regulators cannot force private banks and card networks to join a single system.

- This makes innovation slower and fragmented.

4. Consumer Habits & Culture

- In the West, credit cards are deeply ingrained with reward points and credit lines.

- In India, most consumers prefer direct bank-to-bank transfers (no credit card culture for masses), making UPI natural.

5. Government as a Driver

- UPI was driven as a public good by NPCI (not-for-profit, promoted by RBI).

- In other countries, payments are left to private companies who prioritize profit over inclusion.

- India treated UPI as digital public infrastructure, similar to Aadhaar & JAM trinity.

6. Interoperability by Design

- UPI allows you to pay any bank/any app via the same QR code.

- In the US/Europe, apps like Zelle, Venmo, PayPal, Apple Pay work only within their own closed ecosystems.

- Lack of open standards prevents a UPI-like system from emerging.

7. Scale & Mobile-first Economy

- India’s massive smartphone + cheap data revolution (thanks to Jio) created the perfect environment.

- Many countries don’t have the same scale of smartphone penetration or unified digital ID systems to power instant payments.

✅ In short:

UPI worked because India had government will, regulatory push, public digital infrastructure, and a leapfrog effect skipping cards. Most countries are trapped in legacy payment ecosystems dominated by private networks.

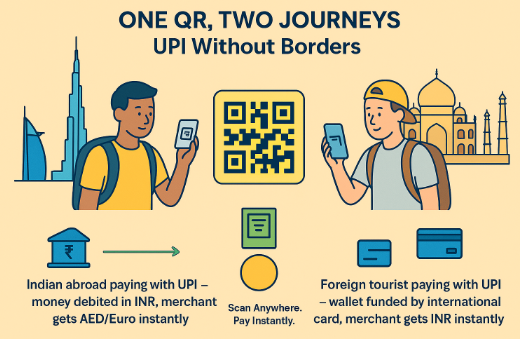

🌍 Can Foreign Tourists Use UPI in India?

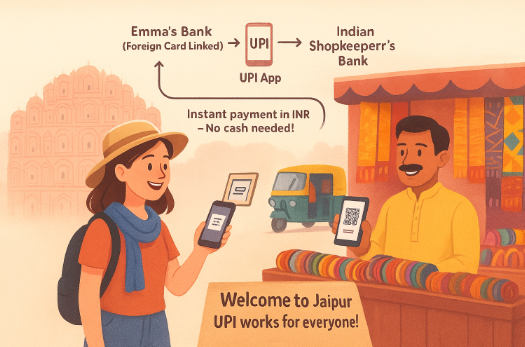

✈️ Story: Emma in Jaipur

Emma, a tourist from London, is shopping in Jaipur’s bustling bazaars. She spots a scarf, the shopkeeper shows a UPI QR, and she wonders: “But I don’t have an Indian bank account!”

Emma hesitates—she doesn’t have an Indian bank account. But here’s the twist: today, even foreign tourists can use UPI in India. She takes out her phone, opens a global fintech app that’s partnered with UPI, scans the QR, and within seconds, the payment goes through—directly from her international card, converted to INR on the spot.

✈️ How It Works for Foreigners

Earlier, UPI was only linked to Indian bank accounts. But since February 2023, NPCI (with RBI’s approval) enabled UPI for international travelers on arrival in India.

Here’s the flow:

- Tourists from select countries (e.g., UK, Singapore, UAE, USA) can set up a prepaid wallet/account with an Indian bank or partner fintech at airports or designated counters.

- That wallet gets linked to UPI, just like an Indian would do.

- Payments happen in Indian Rupees, debited from their wallet (funded by international debit/credit card or forex).

- Merchants get paid instantly in INR, while tourists enjoy the same UPI experience as locals.

🌐 Does UPI Connect to Foreign Banks?

- Directly: No, UPI doesn’t yet pull money straight from foreign bank accounts.

- Indirectly: Yes, via partner apps, wallets, or card networks. For example:

- Singapore’s PayNow is linked with UPI for cross-border transfers.

- NPCI International is signing MoUs with countries like France, UAE, Bhutan, Mauritius, Sri Lanka for UPI acceptance.

- Tourists can also fund Indian UPI-linked wallets through their international Visa/Mastercard.

So Emma’s London bank isn’t plugged into UPI directly, but her international card → Indian UPI wallet bridge makes it seamless.

📊 The Bigger Picture

- In 2024–25, NPCI reported thousands of foreign tourists using UPI wallets during their India trips, especially in metros and tourist hubs.

- India is pushing UPI as an international standard—with live acceptance already in Singapore, UAE, Mauritius, Nepal, Bhutan, and expanding into Europe.

- The vision: whether you’re an Indian abroad or a tourist in India, one QR should just work.

✨ Why This Matters

- For tourists: No need to carry wads of cash or constantly swipe cards with forex fees.

- For merchants: Easy acceptance without extra hardware.

- For India: A powerful branding tool—showcasing digital leadership to every traveler.

🏦 Real Example 1: UPI–PayNow Link (Singapore & India)

In February 2023, India and Singapore connected UPI with PayNow, allowing instant, low-cost transfers between the two countries.

- A Singapore tourist in India can link their PayNow account, send money via UPI, and merchants receive it in INR instantly.

- Similarly, Indians in Singapore can pay merchants through UPI-linked transfers.

This was a world-first in cross-border interoperability—positioning UPI as a global template.

🕌 Real Example 2: UPI in UAE (Dubai & Abu Dhabi)

In August 2023, NPCI International partnered with Mashreq’s NeoPay terminals in the UAE.

- Indian travelers in Dubai can walk into a café, scan a UPI QR at the POS terminal, and pay directly in AED from their Indian bank account.

- This eliminated the need for foreign cards and expensive forex charges.

🗼 Real Example 3: UPI in France

In 2023, NPCI International signed a deal with Lyra, a French payments company.

- The partnership enables UPI acceptance in France, starting with iconic tourist hubs like the Eiffel Tower.

- So soon, an Indian visiting Paris could pay for tickets or coffee using UPI directly.

📊 The India Advantage

- Domestic: Foreign tourists in India can now use UPI by setting up local wallets (launched at airports in 2023).

- International: Indians abroad are already scanning UPI at partner merchants in Singapore, UAE, France, Mauritius, Bhutan, and Nepal.

- Vision: UPI becomes a universal QR standard—whether you’re an Indian abroad or a tourist in India.

✨ So, Emma’s Jaipur shopping trip is just the beginning. In a few years, she might fly home and buy her morning coffee in London using the same UPI QR code—a payment story that started in India, but belongs to the world.

General UPI Transaction Limits

UPI in India has transaction limits set by NPCI (National Payments Corporation of India), and they vary depending on the bank, purpose, and merchant category. Here’s a clear breakdown (as of 2025):

- Per Transaction: ₹1 lakh (₹100,000) is the usual cap for most banks.

- Per Day: ₹1 lakh total across all UPI transactions.

Special Categories with Higher Limits

- Capital Markets, IPOs, Insurance, Mutual Funds, NBFC loan repayments:

👉 Limit increased to ₹2 lakh per transaction. - UPI AutoPay for recurring payments (like OTT, bills, EMI, SIPs):

👉 Limit is ₹15,000 per mandate (for most categories). - Healthcare & Education (as per 2022 RBI circular):

👉 UPI limit extended to ₹5 lakh per transaction.

Merchant/Bank Specific Limits

- Each bank or UPI app (Google Pay, PhonePe, Paytm, BHIM, etc.) can set lower internal limits.

- Example: Some banks cap at ₹25,000–₹50,000 per day, depending on risk/security.

- First 24 hours after adding a new payee, banks often impose stricter limits (like ₹5,000).

✅ In short:

- ₹1 lakh per day for regular users.

- ₹2–5 lakh for special use cases (IPOs, education, insurance, hospitals).

- Bank/app-specific rules may further reduce the cap.

Call to Action

Have you tried UPI while traveling abroad or seen a foreigner pay in India with it? Share your story in the comments!

Do you think UPI should be adopted globally? Tell us what country you’d like to see it in next!

UPI is not just a payment system—it’s India’s digital revolution. Stay tuned as we decode more fintech success stories shaping the world.

Subscribe to our Newsletter for more insights on how India is setting benchmarks in digital innovation.

Read our blogs on Corporate Governance here.

Here’s a well-regarded external reference that highlights the growing international acceptance and expansion of UPI, especially its integration with global platforms:

- PayPal has announced the launch of a cross-border payments platform called PayPal World, linking UPI with major global systems like Tenpay Global (China), Mercado Pago (Latin America), and Venmo—significantly expanding UPI’s international reach. Reuters